Market Update – The End of Another Company Reporting Season

The start of September marks the end of another Australian company reporting season. This is the time of year when public companies report their earnings to investors and CEO’s must get up in front of shareholders and justify their impressive pay packets. Specifically there are two main things that investors want to see in an earnings result. Firstly that companies have been honest about their performance throughout the year, particularly in the lead up to the result, and secondly that they are demonstrating positive earnings momentum in line with stated goals. Inevitably there are always some companies that disappoint, some that surprise on the upside, and some that trudge along as they always have. Disappointing numbers themselves are not necessarily bad, if management can demonstrate that the causes were mostly “one off”. Likewise positive surprises are not always to be celebrated, if the source of the financial outperformance came from non-repeatable earnings. Unsurprisingly CEO salesmanship can have a big impact on how a stock performs post its result. Particularly when their bonuses are at stake!

For this reason it is always important to dig down into the actual numbers, something Libero attempts to do for all our client holdings. Every company is subject to forces within its own sector or industry and needs to be assessed with that in mind. However by looking at the market as a whole, we can also start to get a clearer picture of where things are headed more generally, both from a market investing point of view and from a general Australian economic point of view.

What did this earnings season tell us?

While the ASX200 index itself held up reasonably well, reporting season revealed that underlying growth is soft and patchy. Earnings per share across the index fell by approximately 11%. Despite some weakness being expected due to the ongoing slowdown in the resources sector, it does not appear that non-mining related industries have wholly stepped in to take up the slack, as has been hoped. For example the earnings of industrials shares fell around 1% on average despite hopes for growth aided by the lower AUD. While the construction/housing boom has helped propel some related sectors higher, such as building materials and discretionary retail stocks, outside of that growth has been subdued generally.

The flow on effect of lower earnings is that the ASX200 index is starting to look fully valued by traditional valuation metrics. On a current price to 1 year forward forecast earnings ratio of 16x, the Australian share market is now trading towards the upper end of its longer term historical range, which is closer to 14x forward earnings. While nowhere near the most expensive it has been in the past (eg prior to the tech wreck) the market could not be considered cheap.

Does this mean the market will sell off?

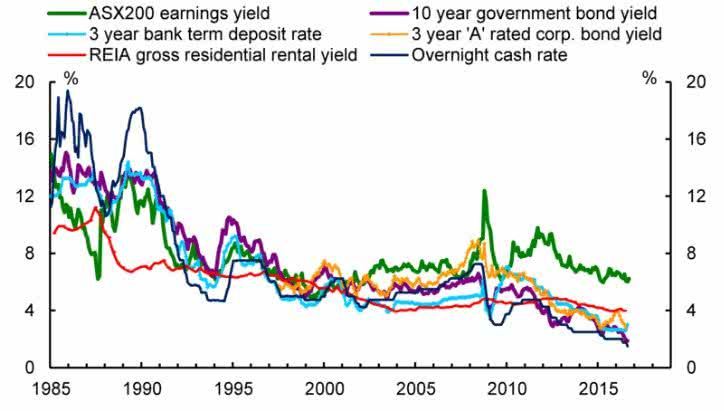

The answer is not necessarily, given the peculiars of the environment we are in. While it may be expensive on an outright earnings basis, it is being buoyed on a relative basis by the fact that it is very difficult to get a positive cashflow return anywhere at the moment, without taking on a greater proportional level of risk. The graph below shows the yield (or income) of traditional income based investments in the current environment. As you can see all of them are at record lows due to ultra-low interest rates globally. On a relative basis the yield on shares is actually holding up considerably well, which is why the Aussie market is finding such strong valuation support even given the lacklustre earnings. The story is also similar for global shares (although the US market is being driven slightly more by earnings growth than yield).

A low return environment

For the time being unfortunately it appears we are stuck in a lower return environment, which is likely to continue until we start to see a sustained recovery in economic growth globally. The great hope of central banks and governments is that low interest rates (officially known as “accommodative monetary policy”) will drive people to spend (and businesses to invest) rather than save and earn very little interest. Unfortunately however the hangover from the financial crisis is still with us. Consumer nervousness, political populism, structural issues, demographic changes and high private debt levels are all weighing on consumer and business sentiment. And it will likely take some time for these issues to be worked through.

In the meantime however the most prudent tactic is to retain a strong focus on diversification and to avoid the temptation to move further out along the “risk curve” into more speculative or overvalued assets in order to generate higher returns. While doing so can temporarily result in outperformance, this strategy can backfire pretty quickly during times of crisis or uncertainty, particularly as these assets can be hard to offload. We are seeing evidence of this trend starting to occur given the high valuations of “long duration” assets, such as certain Real Estate Investment Trusts.

Libero is currently in the process of rebalancing portfolios based on the outcomes and analysis from company reporting season. If you have any queries, or wish to discuss the current investment environment, please don’t hesitate to call.

Glen Holder, BCom, DipFP, CA, MAppFin

Director – Investment Management